Giuseppe Paleologo recently released a draft version of his forthcoming book. It's good!

The Elements of Quantitative Investing

Before the Trade

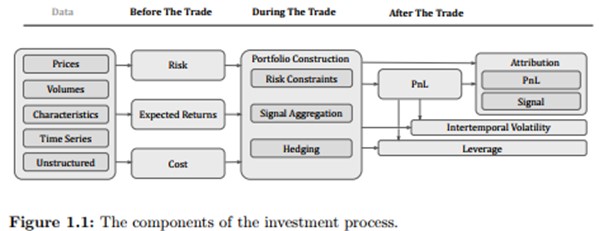

Chapter 1: Gappy introduces core financial instruments like bonds, equities, and futures, making them accessible to beginners. He explains the concept of excess returns, illustrating how certain strategies outperform market averages. The chapter closes with a clear diagram (fig. 1.1) of the investment process in quantitative investing, which provides a solid foundation. More specific examples of successful strategies would enhance the discussion, but overall, the balance between theory and application is well-structured.

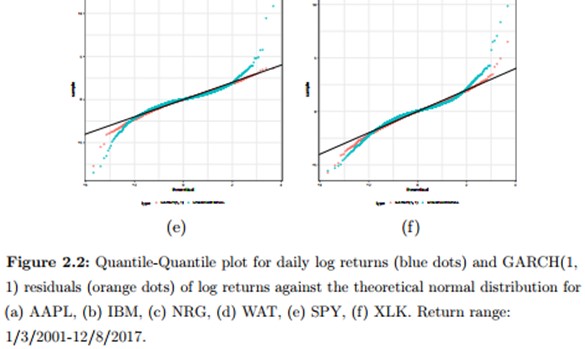

Chapter 2 focuses on types of returns and introduces volatility models, notably the GARCH model. Graphical (fig 2.2) and mathematical examples help clarify these concepts, while state-space models like EWMA and the Harvey-Shepherd model add depth. The section on the Kalman filter adds an insightful tool for dynamic model adjustments. More real-world applications of GARCH and Kalman filter use cases would strengthen practical understanding, making the chapter more engaging.

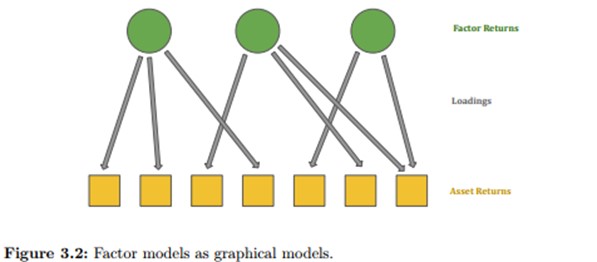

Chapter 3: Gappy explains factor models and their practical applications for managing portfolio risk. Supported by diagrams (fig. 3.2), the chapter explores transformations of these models and introduces different types, such as macroeconomic and fundamental factors. The balance of theory and practice is strong, but additional real-world scenarios would enhance the material further.

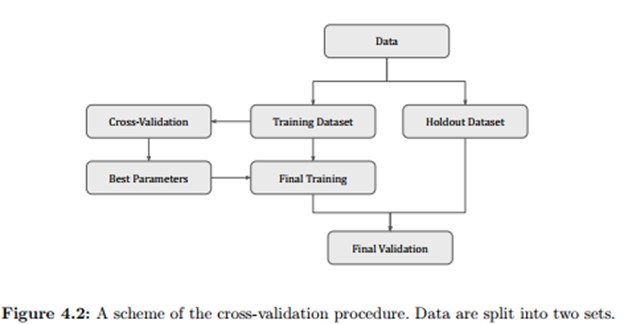

Chapter 4 centres on backtesting, Gappy outlines best practices and protocols essential for validating trading strategies. The use of flowcharts (fig. 4.2) enhances clarity, making the processes easy to follow. He presents a detailed look at the Rademacher anti-serum, capturing the reader’s attention with its structured approach.

Chapter 5 examines robust loss functions and their applications to multivariate returns. Gappy skillfully explains precision matrices and minimum-variance portfolios, as well as concepts like Mahalanobis distance. The chapter concludes by addressing ancillary tests, including beta and the coefficient of determination. The theoretical discussions are well-articulated, but providing clearer connections between these mathematical concepts and their implications for risk management would be helpful.

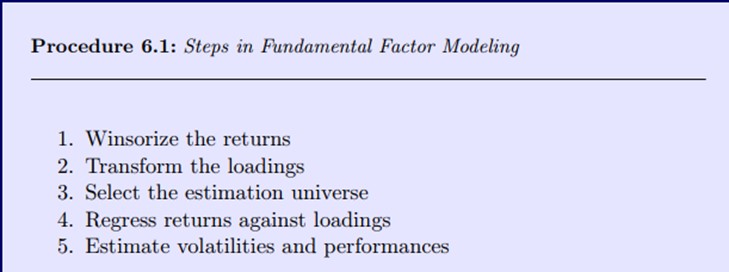

Chapter 6 dives into factor models, Gappy focuses on their inputs and processes while explaining cross-sectional regression and factor covariance matrices. He presents detailed procedures (proc. 6.1), leading to a discussion on winsorization of returns. The content throughout the chapter is thorough and leaves the reader with a much greater grasp of factor models.

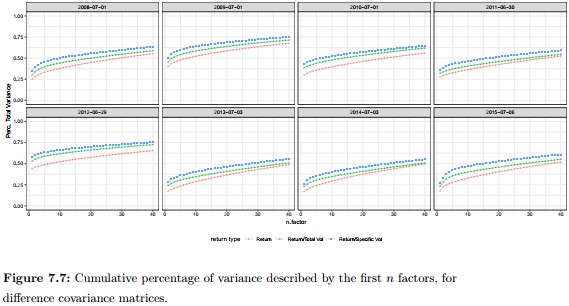

Chapter 7 extends upon factor models, introducing statistical factor models, with advanced topics like principal component analysis (PCA). The comparison of PCA with spiked covariance models is particularly effective, aided by illustrative graphs (fig. 7.7). While the chapter is engaging, discussing the implications of these statistical methods in portfolio construction would further enrich the content.

During the Trade

Chapter 8: Gappy now moves to the second part of the book, During the trade, and explores portfolio management by introducing mean-variance optimization and its implications for different portfolios. He emphasizes key concepts like trading in factor and idiosyncratic spaces while discussing diversification strategies and the information coefficient performance ratio. While the content is well-organized, a more thorough exploration of the limitations of mean-variance optimization could add depth to the analysis.

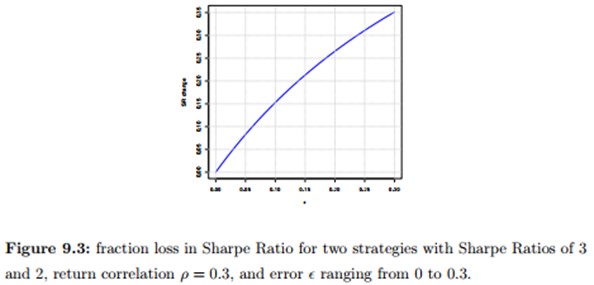

Chapter 9 critically assesses the naïve mean-variance optimization model, highlighting how constraints and estimation errors can significantly impact model performance, supported by visual illustrations (fig. 9.3). Gappy presents thought-provoking commentary on Sharpe ratios, showing how a lower Sharpe ratio doesn’t necessarily lead to lower returns.

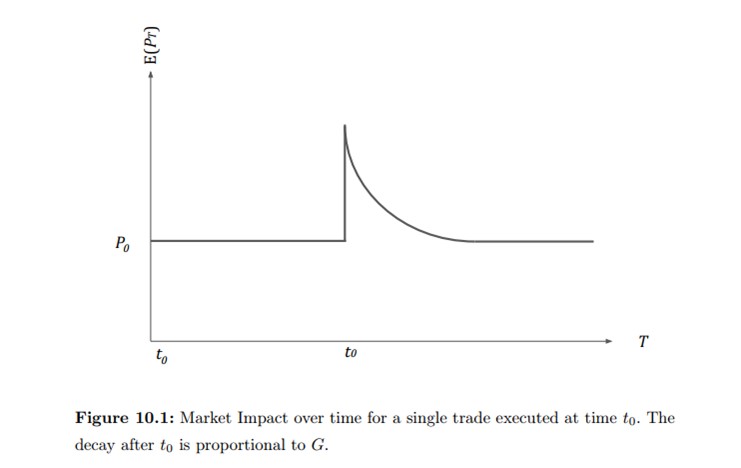

Chapter 10 examines the market impact of transaction, utilizing visuals (fig. 10.1) to clarify key points. The chapter includes a discussion on multiperiod optimization and delves into the Baldacci-Benveniste-Ritter model, making complex concepts accessible.

Chapter 11 transitions to hedging strategies, Gappy presents a comprehensive overview, beginning with general principles before moving to time-series hedging and the concept of factor-mimicking portfolios. The chapter employs exercises (ex. 11.2) that aid understanding. The clarity of explanations is commendable, yet a broader discussion of the theoretical underpinnings of various hedging strategies would strengthen the overall narrative.

After the Trade

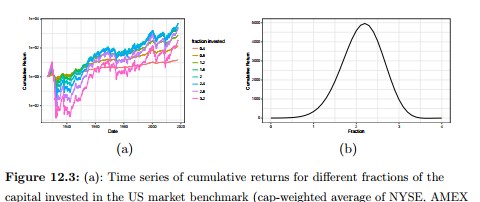

Chapter 12: Gappy now moves on to the final part of the book, where he explores the Kelly criterion, employing various illustrations (fig. 12.3) to clarify its mathematical foundations and practical implications. The intuitive explanations surrounding Kelly strategies, including fractional Kelly, make for an engaging read. However, elaborating on the theoretical challenges associated with implementing these strategies could offer readers a more rounded perspective on their application.

Chapter 13: The concluding chapter centres on performance attribution, distinguishing between skill and luck in model outcomes. Gappy’s examination of idiosyncratic profit and PnL provides a thoughtful resolution to the book’s themes. These discussions are well-structured and insightful and round out the reader’s understanding of quantitative investing.